By Steven Wiseglass | First published April 2025. Last updated May 2026.

Trading whilst insolvent is a serious matter that can have significant legal, financial, and reputational consequences for company directors, shareholders, and the business itself.

This guide explains what trading whilst insolvent actually means, the three legal tests that determine whether your company is insolvent, the consequences directors face, and — critically — what you should do right now to protect your personal position.

When is a Company Technically Insolvent?

A company is technically insolvent when it cannot pay its debts as they fall due, or when its total liabilities exceed its total assets. Under the Insolvency Act 1986, there are three formal tests directors should apply. Failing any one of them means your company is likely insolvent and professional advice should be sought immediately.

The three tests in question are:

- Cash Flow Test: If a company cannot pay its debts as they become due, for example, if it cannot pay suppliers, employees, or HMRC on time, it may be considered cash flow insolvent.

- Balance Sheet Test: This occurs when a company’s liabilities have exceeded the value of its assets. If your balance sheet shows negative net assets, your company is balance sheet insolvent.

- Legal Action Test: There is a third test directors often overlook. If a creditor is owed £750 or more and has served a formal statutory demand, and your company has failed to pay, secure the debt or apply to set it aside within 21 days, this constitutes legal proof of insolvency. A County Court Judgment against the company has the same effect.

| Test | What it measures | Warning signs |

| Cash Flow Test | Can the company pay debts as they fall due? | Missed supplier payments, late PAYE, HMRC chasing, overdraft at limit. |

| Balance Sheet Test | Do liabilities exceed assets? | Negative net assets on balance sheet, loans exceeding asset values |

| Legal Action Test | Has a creditor taken formal action? | Statutory demand received, CCJ issued, winding-up petition filed |

If your company fails any one of these tests, it is likely insolvent. Failing more than one significantly increases your personal risk as a director.

Directors are expected to prevent their company from trading whilst insolvent if they know, or it is deemed that they should have known, the company is insolvent. By continuing to trade whilst insolvent, the director exposes themselves and the business to serious risk.

What is Trading Insolvent?

Trading insolvent means a company is continuing to operate and taking on new debts despite being unable to pay its existing liabilities. It is a clear indicator of financial distress and one of the most serious situations a director can face because it is the point at which personal liability begins to attach.

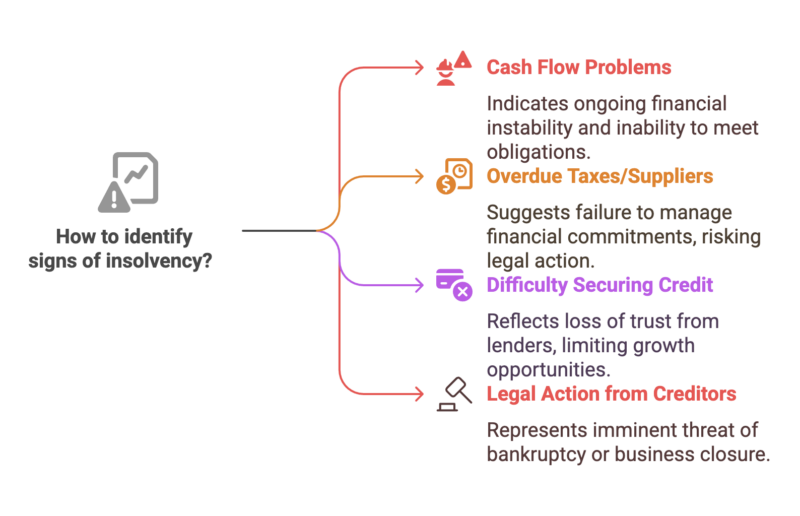

Some of the common warning signs of insolvency are:

- Persistent cash flow problems.

- Overdue taxes or unpaid suppliers.

- Difficulty securing credit or loans.

- Legal action from creditors, such as winding-up petitions.

Consequences of a Limited Company Trading Whilst Insolvent

The consequences of trading whilst insolvent can be severe. They range from personal liability for company debts and director disqualification, through to criminal prosecution in the most serious cases. The severity depends on how long trading continued after insolvency was known or should have been known, and whether the director took steps to minimise losses to creditors.

The table below summarises the key risk factors and their likely outcomes. Directors should assess honestly which of these situations apply to their company right now.

| Action | Risk level | Possible outcome |

| Continuing to trade with no recovery plan. | High | Personal liability for all debts incurred from point of insolvency. |

| Paying connected parties or family ahead of other creditors. | High | Payments reversed by liquidator, personal liability. |

| Selling assets below market value. | High | Transaction reversed, director ordered to make up shortfall. |

| Taking on new credit with no prospect of repayment | High | Fraudulent trading allegation, potential criminal prosecution |

| Taking early advice from a licensed IP | Low | Demonstrates responsible conduct, limits personal exposure |

| Documenting all decisions with board minutes | Low | Provides defence against wrongful trading allegations |

Each of these risks is examined in detail below — starting with the most common consequence directors face, and escalating through to the most serious.

1. Wrongful Trading Liability

As per the Insolvency Act 1986, directors have a legal duty to act in the best interests of creditors when their company is insolvent. If a director continues trading despite knowing they are insolvent, or that insolvency is unavoidable, they can be held personally liable for increasing company debts. This is a key aspect of a company director’s liability for insolvent trading.

It’s important to note that wrongful trading does not require fraudulent intent — it simply refers to continued operations when there is no reasonable prospect of recovery. If the company were to enter liquidation, the liquidator will investigate whether the director acted responsibly. If proven guilty of wrongful trading, they may be required to personally contribute to repaying company debts.

2. Personal Liability for Company Debts

Directors are usually protected by limited liability. This means that, ordinarily, company debts do not affect the personal finances of directors. However, if one is found guilty of wrongful or fraudulent trading, this protection may be removed.

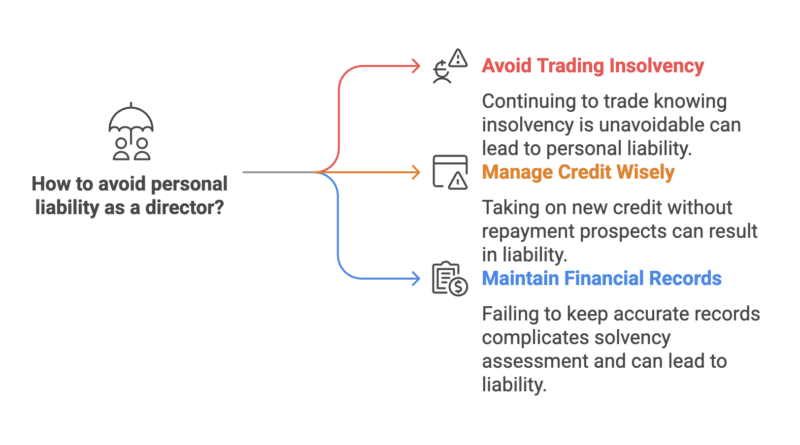

A director may be deemed personally liable if they:

- Continue to trade knowing insolvency is unavoidable.

- Take on new credit without the prospect of it being repaid.

- Fail to keep accurate financial records, making it harder to assess company solvency.

3. Director Disqualification

If a limited company trades whilst insolvent, directors can face disqualification under the Company Directors Disqualification Act 1986. This results in a ban from acting as a director or holding a management position in any company for up to 15 years.

Disqualification may be sought if:

- The director fails to minimise creditor losses.

- There is evidence of mismanagement and/or financial misconduct.

- The company’s records show signs of wrongful or fraudulent trading.

A disqualification order can severely impact a director’s future post-insolvency and liquidation of their business. Breaching a disqualification order could even lead to criminal prosecution.

However, in some circumstances, it may be possible for a disqualified director to be able to act as a shareholder. For more information on this process, read our dedicated blog.

4. Legal Action from Creditors

When a company is not able to pay its debts, creditors have the right to take legal action in order to recover what they are owed. The most drastic step creditors can take in this scenario is the issuing of a winding-up petition, which can lead to enforced liquidation if a winding-up order is issued. This will result in assets being sold to repay debts, and the business being closed.

Other measures creditors could take include:

- Seeking County Court Judgements (CCJs): Makes it significantly harder to obtain future finance.

- Apply for a Statutory Demand: Statutory demands require payment within 21 days before escalation.

- Enforcement: Asset seizure via bailiffs/enforcement agents.

5. Forced Liquidation of the Company

When an insolvent company continues trading, despite its status, it can expect to be placed into compulsory liquidation in short order. This can happen through a number of different ways:

- A creditor’s winding-up petition as a result of unpaid debts.

- A court order, following an investigation into suspected wrongful trading.

- Director-initiated liquidation, if they assess the situation and accept the business is no longer a viable entity.

When in liquidation, the company’s assets will be seized and sold in order to repay creditors. The business is then removed from the Companies House register — meaning it officially ceases to exist.

6. Potential Criminal Charges for Fraudulent Trading

Company directors found guilty of committing misconduct in the lead up to insolvency could face charges of fraudulent trading under Section 213 of the Insolvency Act 1986.

Scenarios that could lead to accusations of fraudulent trading include:

- Deliberately misleading creditors.

- Falsifying financial information.

- Attempting to hide assets.

Fraudulent trading effectively refers to any scenario where a company incurs debts without any obvious ability, or intention, to ever repay it. Authorities take fraudulent trading extremely seriously. Any attempts made to deceive creditors can have serious legal consequences, including:

- Prison sentences of up to 10 years.

- Lifetime director bans.

- Unlimited fines, to be determined by the severity of the fraud.

Concerned about your personal exposure as a director? Download Inquesta’s free fact sheet A Guide to Avoiding Director Exposure for a clear overview of where directors become personally liable and the steps you can take to limit your risk.

How Does a Liquidator Prove Wrongful Trading?

A liquidator proves wrongful trading by examining the company’s financial records, payment history, and director conduct in the period leading up to insolvency. They are looking for evidence that directors knew — or should have known — the company was insolvent, and failed to act in creditors’ interests. Here is exactly what they examine.

- Company Accounts & Cash Flow Records: When did the company first show signs of insolvency? Were management accounts being produced? Did the directors have visibility of the financial position?

- Timing of Payments: Were creditors being paid selectively? Did the company continue paying directors’ salaries or dividends while HMRC and trade creditors went unpaid?

- Director Loan Accounts: Were drawings made from the company when it was already insolvent? Overdrawn director loan accounts are one of the most common issues liquidators pursue.

- New Debts Incurred: What credit was taken on after the point of insolvency? Were suppliers, lenders, or HMRC allowed to extend credit that the director knew could not be repaid?

- Correspondence With Creditors & Advisors: Were warning letters ignored? Was professional advice sought and acted upon, or disregarded?

- Board Meeting Minutes: Were formal discussions held about the company’s financial position? Were decisions documented and defensible?

The most important protection a director has is a clear paper trail demonstrating they took the situation seriously, sought professional advice, and made decisions in creditors’ interests.Is your company trading whilst insolvent, or do you suspect it might be? Every week of delay increases your personal exposure. Inquesta is a licensed insolvency practice led by Steven Wiseglass — IPA regulated, Fellow of R3, over 20 years of experience helping directors understand and manage their position before liquidators become involved. Call 0800 093 4604 for a confidential, no-obligation assessment. There is no pressure and no judgement — just honest advice about where you stand.

What Should Directors Do?

If your company is insolvent or approaching insolvency, you must act immediately. The options available to you today— (Time to Pay arrangement, a CVA, administration, or a CVL) may not be available in three months. Every week of inaction narrows your choices and increases your personal exposure. Here is what you need to do now.

Seeking professional advice from a licensed insolvency practitioner is the most protective step a director can take. Instructing a licensed IP demonstrates you took the situation seriously and sought expert guidance. If the company later enters liquidation, this is one of the strongest defences against wrongful trading allegations. Do not wait until creditors have issued statutory demands or filed winding-up petitions.

Start documenting every decision from the moment you identify your company may be insolvent. Every significant business decision should be recorded in board meeting minutes. This includes salary adjustments, changes to payment priorities, discussions about recovery options, and any professional advice received and acted upon. A liquidator will look for evidence of responsible decision-making. Your documentation is that evidence.

Stop making preferential payments. Do not pay connected parties (family members, directors, or related companies) ahead of trade creditors or HMRC. These payments can be reversed in liquidation, and you can be held personally liable for allowing them. All creditors must be treated equally.

Explore formal insolvency options. Depending on your specific circumstances, several formal procedures may be available. A Time to Pay arrangement with HMRC can resolve tax debts and allow continued trading. A Company Voluntary Arrangement (CVA) enables the business to continue operating while repaying creditors over an agreed period. Administration provides legal protection from creditor action while a rescue plan is developed. If the business cannot be saved, a Creditors’ Voluntary Liquidation (CVL) allows an orderly wind-down that minimises personal risk and demonstrates responsible directorship.

Do not dissolve the company to avoid debts. This is not a viable route if debts exist. Creditors will object, the Insolvency Service has expanded powers to investigate dissolved companies retrospectively, and directors can face personal liability and disqualification regardless of dissolution

💡 From an Expert Insolvency Practitioner

Steven Wiseglass

Director | Licensed Insolvency Practitioner

Founder, Inquesta | 10+ years in practice | Fellow of R3 | Member, R3 North West Committee

“The directors who come to us in the best position are the ones who called early, took advice, and kept records. They can show the liquidator exactly what they knew, when they knew it, and what they did about it. The ones in the worst position are those who knew something was wrong, didn’t seek advice, and kept trading hoping things would turn around. By the time we speak to them, they often have months of personal liability exposure they didn’t need to have. The call to an insolvency practitioner costs nothing. The alternative can cost you everything.”

Frequently Asked Questions

Is trading whilst insolvent illegal? Trading whilst insolvent is not automatically a criminal offence. It becomes a civil offence, known as wrongful trading, when directors continue trading after they knew insolvency was unavoidable and fail to minimise losses to creditors. Deliberate fraud takes it into criminal territory.

If fraudulent intent is involved (falsifying records, hiding assets, deliberately misleading creditors) it becomes fraudulent trading under Section 213 of the Insolvency Act 1986, carrying potential prison sentences of up to 10 years, lifetime director bans, and unlimited fines.

Can I continue trading if my company is insolvent? In limited circumstances, yes — but only if you have a clear, viable recovery plan and can demonstrate you are actively protecting creditors’ interests. Without professional advice and documented decision-making, continuing to trade once insolvent significantly increases your personal liability exposure.

Every decision made after the point of insolvency will be scrutinised by a liquidator if the company later fails. The question they will ask is whether continuing to trade was genuinely in creditors’ interests, or whether it simply delayed an inevitable outcome while debts mounted.

What is the difference between wrongful trading and fraudulent trading? Wrongful trading is a civil offence under Section 214 of the Insolvency Act 1986. It requires no fraudulent intent, only negligence. Fraudulent trading under Section 213 is a criminal offence involving deliberate deception of creditors. The legal threshold and consequences are significantly different.

Wrongful trading can result in personal liability for company debts and director disqualification. Fraudulent trading carries criminal prosecution, potential imprisonment, and unlimited fines. Directors who acted negligently but not dishonestly face civil consequences. Directors who deliberately deceived creditors face criminal ones.

Can an insolvency practitioner force me to cease trading? No. If you voluntarily consult with a licensed insolvency practitioner, the decision to continue or cease trading remains entirely with you as a director. An IP advises. They cannot force your company into a formal insolvency procedure at a consultation.

What they can do is give you an honest assessment of whether continuing to trade is defensible, and what steps you should take to protect yourself if you do continue. Taking that advice, and acting on it, is one of the strongest protections available to a director in this position.

What can I do to protect myself if my company is insolvent? The most important steps are to seek advice from a licensed insolvency practitioner immediately, document all significant decisions in board meeting minutes, stop making preferential payments to connected parties, and explore formal options such as a CVA, administration, or CVL.

Directors who can demonstrate they acted responsibly, sought professional advice, and made decisions in creditors’ interests are in a far stronger position if the company later enters liquidation. A clear paper trail is your primary defence against wrongful trading allegations.

Don’t Wait Until It’s Too Late

Trading whilst insolvent is one of the most serious situations a company director can face. Fortunately though, it it is manageable if you act quickly and get the right advice. The directors who face the most damaging personal consequences are almost always those who waited, hoping things would improve, while their personal liability grew with every week of continued trading.

The options available to you today (a Time to Pay arrangement, a CVA, administration, or a controlled CVL) may not be available in three months. Inquesta is a licensed insolvency practice led by Steven Wiseglass, IPA regulated and Fellow of R3, with over 20 years of experience helping directors in exactly this position. Call 0800 093 4604 or fill in our contact form today for a confidential, no-obligation assessment of your situation. The sooner you act, the more choices you have.

This article is for informational purposes only and does not constitute legal or financial advice. For tailored advice, please consult a qualified insolvency practitioner.

💡 From an Expert Insolvency Practitioner

Steven Wiseglass

Director | Licensed Insolvency Practitioner

Founder, Inquesta | 10+ years in practice | Fellow of R3 | Member, R3 North West Committee

“Most directors we speak to knew their company was struggling for months before they called us. What they didn’t realise was that the moment they could identify their company was insolvent — whether that’s missing a VAT payment, receiving a statutory demand, or seeing a negative balance sheet — their legal duties changed.

From that point, every decision they made as a director is scrutinised against one question: did they act in the best interests of creditors? Directors who can answer yes to that question are in a defensible position. Directors who can’t are facing personal liability.”